Private Forms of Money and the State [Part II]

On the ongoing entanglements from QE via crypto and through the shadow to digital monies: or there and back again

Image created with Apple Image Playground and Bazaart (2025).

[Work in progress]

In the previous post it has been shown how private monies can be broadly characterised vis-à-vis public money. In the following it is to be explained how private forms of money have shaped public forms of money and vice versa, i.e. how monetary and fiscal policy developments of states (together with the unfolding un/intended consequences in the economy) have given rise to new forms of private money.

Quantitative Easing constitutes money creation, purchases of crypto are asset swaps

The first part of this introductory investigation into the relationship between private money and the state has ended upon the notion that cryptocurrencies have developed as a reaction by private entrepreneurs in response to the GFC. In particular, it can be argued that states’ policy response through their central banking systems’ Quantitative Easing (QE) approach triggered the attempted technological fix by private entrepreneurs via the development of cryptocurrencies. Although this may be a valid reflection of the historical chain of events unfolding post-GFC, it does not address the subtleties that both response approach entail and differentiate from each other. While QE constitutes a monetary policy instrument by central banks involving the purchase of government bonds in the secondary market and an act of money creation (similar to the emission of government bonds on the primary market), cryptocurrencies do not involve the creation of legal tender money (i.e. state issued currency) as the purchase of cryptocurrency shows itself a trade of legal tender (public) money for technically (and privately) created digital coins or tokens. The latter transaction is also called an asset swap. The same goes for stablecoins. Stablecoins attempt to peg their value to a fiat-currency in order to resemble it ‘by holding mostly fiat-denominated short-term assets, such as treasury bonds, high-quality commercial paper, repurchase agreements and bank deposits’. To argue that stablecoin trades are to be categorised as an asset swap seems to go against a Federal Reserve paper, which says:

“Funds flowing into stablecoins have to flow out of another source. […] This potential flow of funds from bank deposits into stablecoins could increase Treasury demand but also could reduce the supply of loans in the economy. […] This potential flow of funds from bank deposits into stablecoins could increase Treasury demand but also could reduce the supply of loans in the economy.” [1]

Taking this quote at face value, the argument is notably building upon the ‘loanable funds theory’. First, to claim that the purchase of stablecoins with bank deposits would ‘reduce the supply of loans in the economy’ is based on the assumption that banks can only lend if they are successful in the acquisition of private sector deposits beforehand. As shown in a critical appraisal of the three main theories of banking previously, banks do neither require deposits nor reserves a priori in order to lend and do however engage in the lending business in accordance with their internal growth strategy (incl. their expenditure and earnings calculus), with their risk appetite with regards to the creditworthiness of loan candidates as well as with the overall dynamic in the credit market and general loan demand. [2] Banks rather create deposits when issuing loans (which is more in line with the credit creation theory of banking) and care about the funding via deposits or reserves a posteriori (in the Latin sense of the word), i.e. at a later stage [3]: ‘buying stablecoins with deposits does not decrease lending by banks’. [4] Second, a ‘flow of funds from bank deposits into stablecoins’ does hence not increase the demand for Treasury bills:

“The stablecoins issuer ‘collects’ deposits and then buys Treasuries on the secondary market. However, this means that someone […] is selling Treasuries and ‘cashing’ deposits. At the aggregate level, nothing changes. The deposits have moved from one private [person] to another […]. Treasuries moved from a private individual […] to the stablecoins issuer. So buying stablecoins with deposits does not increase the demand for Treasuries. It is an asset swap.” [5]

This topic shows that central banks themselves are complex institutions whose staff exhibit a variety of views. Whether investments in stablecoins affect the demand for Treasury titles should be empirically investigated and determined. Needless to say, the juxtaposition of Quantitative Easing (QE) and stablecoins’ entanglement with treasury bonds enhances the key differences by nature (and not only in kind).

Banking in the shadows, dragged into the regulated open by crises?

This shows, however, again, how private money initiatives such as cryptocurrencies were first unregulated practices of financial innovation and rather exclusive financial instruments, but became integrated into the architecture of the financial system over time. In Europe, the MiCA Regulation (EU) 2023/1114 was adopted to regulate the market in crypto assets and to protect users and investors alike. The national supervisory authorities as well as the European supervisory authorities for banking supervision (EBA), insurance (EIOPA), and securities and financial markets (ESMA) have jointly developed an interactive information sheet featuring explainations of technical terms (electronic money tokens = EMTs, asset-referenced tokens = ARTs, crypto-assets other than EMTs and ARTs) in a simple and easy-to-understand way by providing also an overview of the crypto-assets that are being regulated under MiCA. [6] In the course of the years following the Great Recession, public monetary responses (QE) to the unbridled private financial innovations (mortgage-backed-securities, MBS; collateralised debt obligations, CDO; CDO-squared) in the pre-2008 period led to the advancement of cryptocurrencies. What about other forms of private monies that impact our monetary systems long before the advancement of cryptocurrencies?

Since the establishment of the Bretton Woods system after WWII, the international monetary system has been highly regulated resulting in restricted business activities for international banks that were mostly London-based in an era where the British pound dominated as the world’s reserve currency before the outbreak of war:

“By the end of the war, the US dollar had replaced the British pound as the international reserve currency. However, the US banking system was still quite provincial and lagged behind the international role of the US dollar (Helleiner, 1994). British bankers saw an opportunity in this discrepancy: they began to grant loans in US dollars against their growing US dollar deposits from international customers (Schenk, 1998). In other words, they began to create US dollars, i.e. to establish a dollar market in Europe, which is why it is still called the “Eurodollar market” today. The Bank of England enabled business in US dollars by accepting a new accounting technique: financial transactions in which all parties were non-residents were to be considered “offshore” and not subject to national financial regulation. All other transactions would be “onshore” and regulated by the Bank of England (O’Malley, 2015). With this accounting technique, the term “offshore” found its way into banking jargon.” [7] (own emphasis)

This practice of offshore money creation, ‘in which banks accept deposits and issue loans denominated in foreign currencies, can be understood as a form of shadow banking system at the international level’. [8]

Def.: Offshore

“term for a new, specific form of cross-border financial transaction:

one that was only offered to non-residents (principle of non-residency),

was subject to little or no taxation and was largely unregulated, and

was invisible outside the exclusive circle of participating bankers.” [9]

It is this transnationality aspect that ‘changed the nature of modern money in that the underlying general debt relationship now extended across borders and jurisdictions’ compared with the situation in the period between the 17th century and WWII when ‘the state and domestic banks had shared the power of money creation’ and ‘now this power was extended to foreign banks’. [10]

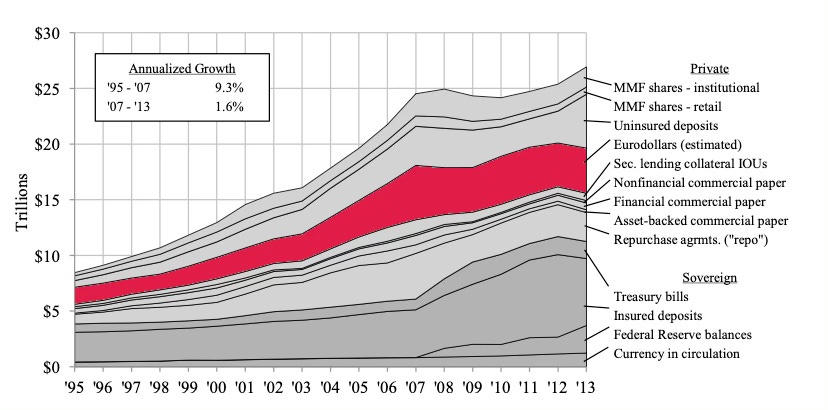

The offshore / eurodollar market is a rather significant part of the private monetary security structure, by which is meant the political process to equip certain actors with the license to create money. [11] The chart below shows the evolution of US dollar-denominated short-term debt (for asset classes for which data is available) since 1995 (in gross quantities and maturity cutoff being one year):

US dollar-denominated gross money-claims outstanding, 1995-2013

Note: The coloured series shows the estimated Eurodollar claims (added own emphasis).

© Ricks (2016, p. 33)

The chart depicts private money-claims (lighter shading) as well as the sovereign (publicly backed) money-claims (darker shading). The market for US dollar denominated money-claims (demandable up to one year) more than doubled in less than two decades exceeding US$25 trillion on a gross basis by 2013. It is thus much larger than total outstanding US mortgage debt standing at about US$14 trillion that year. [12] It is also worth noting that this market is primarily an institutional and not a retail one: ‘apart from deposits, MMF shares, and physical currency, very few of these instruments are held directly by individuals’. [13]

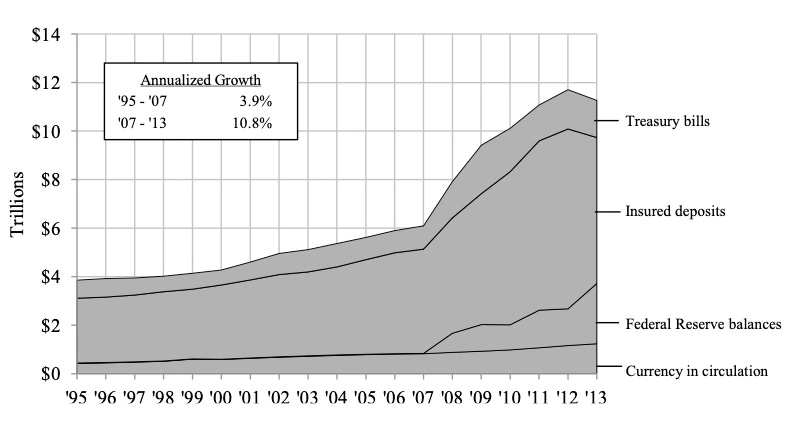

US dollar-denominated gross sovereign money-claims outstanding, 1995-2013

© Ricks (2016, p. 35)

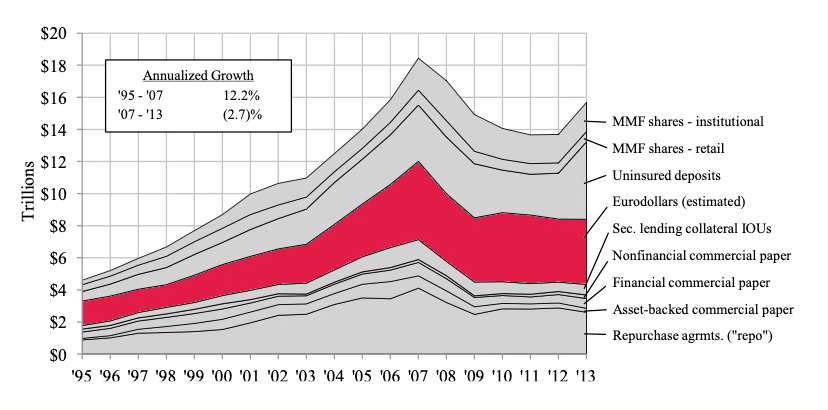

Comparing the US dollar-denominated gross sovereign money claims (above) with the solely private components of this asset class (below), it can be recognised that the annualised growth rates of the private (12.2%) far outpaced the sovereign one (3.9%), especially in the period leading up to the GFC:

US dollar-denominated gross private money-claims outstanding, 1995-2013

Note: The coloured series shows the estimated Eurodollar claims (added own emphasis).

© Ricks (2016, p. 34)

This tend reversed itself after 2007, when the private aggregate plummeted and the sovereign one stepped in with the US government’s and Federal Reserve’s interventions meaning to prevent the what was to be called Great Recession turn into another (far worse) Great Depression. [14] The massive post-crisis contraction of private money-claims has not significantly been compensated by the Federal Reserve’s balance sheet expansion (Federal Reserve balance + currency in circulation) but mostly (but not completely) by ‘emergency increases in deposit insurance coverage’:

“This increased coverage was attributable to two policy measures: first, the statutory increase in the deposit insurance cap from $100,000 to $250,000 (see Emergency Economic Stabilization Act of 2008 § 136, 12 U.S.C. § 5241; Dodd-Frank Wall Street Reform and Consumer Protection Act, Pub. L. No. 111- 203, § 335, 124 Stat. 1376, 1540 (2010)); and second, the Federal Deposit Insurance Corporation’s Transaction Account Guarantee, which temporarily removed the deposit insurance cap for noninterest-bearing demand deposit obligations (see 12 C.F.R. § 370.4). The termination of the latter program is responsible for the uptick in uninsured deposits and the corresponding downtick in insured deposits after 2012.” [15]

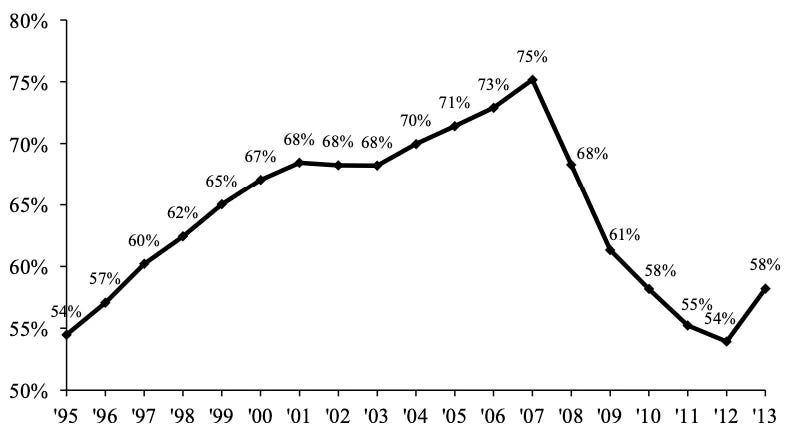

US dollar-denominated gross private money-claims as percentage of total, 1995-2013

© Ricks (2016, p. 35)

The contraction of private money-claims expressed as a share of the total meant a drop from its peak at 75% in 2007 to 54% five years later returning to the point of departure of this period under view in 1995:

“The increasing private share from 1995 to 2007 can be understood as an increasing privatization of the broad money supply in the precrisis years. […] [F]or at least the past two decades, practically all money- claims have been issued by the financial sector and the government. That is to say, nonfinancial (commercial or industrial) issuers have been virtually nonexistent. […] [N]onfinancial commercial paper—represents issuance by commercial or industrial firms. And that market is trivial.” [16] (own emphasis)

This shows how critical private money creation became and continues to be. It is concerning how little attention is generally granted to private money creation compared with the near fetishistic focus on sovereign money creation, and even more so how fast the shadow banking sector grows without any considerable political attention properly dedicated to it. While the domestic monetary security structures consist of commercial banks’ ability to trade their liabilities (i.e. loan commitments) ‘at par’, i.e. ‘at a one-to-one exchange rate with the liabilities of the central bank’, shadow bank liabilities lack ‘explicit public backstops’ such as ‘public supervision, deposit insurance, and lender-of-last-resort guarantees’. [17]

Call for more integrated regulation of market-based finance

This insight has also been articulated in part by the chair of France’s Autorité des Marchés Financiers calling in the Financial Times for a European level supervision of market-based finance that includes issuers of cryptocurrencies and stablecoins:

“Because the current system is largely sub-optimal. Where financial stability is concerned, it is never good to split responsibilities among several supervisors. Since market-based finance now accounts for half of international finance, it matters more than ever to make sure that someone is clearly in charge of overseeing the largest entities through consolidated supervision. […] Take the rapidly evolving cryptoasset sector. Cryptoasset distribution is inherently cross-border and fast-moving. But Esma has no direct powers while each of the 27 regulators has to develop its own competences, and can decide to grant a licence and the passport to address clients throughout the EU. […] Cryptoassets platform operators can typically ‘shop around’ national regulators, fuelling damaging ‘regulatory forum shopping’. Esma needs direct supervision of global pan-European cryptoasset service providers as a matter of urgency.” [18] (own emphasis)

In other words, when only one member-state of the European Economic and Monetary Union (EMU) granted in the current divergently interpreted regulatory landscape among member states a MiCA licence to an issuer of US dollar stablecoins, such as US dollar Coin (USDC) issued by Circle for instance [19], it would mean that those Eurodollar USDCs are compliant in the whole EU and can be redeemed in Europe (according to the so-called “fungibility principle”) and undermine European monetary sovereignty in the process:

“Eurodollar stablecoins are a type of stablecoin pegged to the U.S. dollar but used outside the US and its direct regulatory jurisdiction. […] Eurodollar stablecoins offer stronger redemption rights and stricter pegging/reserve requirements, leaving the EU vulnerable to runs and necessitating close, potentially subordinating, coordination with US authorities. Fungibility raises the critical question of “moneyness”, the credibility of the promise to redeem the stablecoin at par on demand. This promise is not uniform. Regulatory asymmetries create a hierarchy of moneyness: a Eurodollar stablecoin operating under the more stringent MiCAR regime offers a stronger, more credible promise. MiCAR mandates issuers to offer par convertibility on demand for all owners, whereas in the US, the GENIUS Act allows tiered redemption: institutional owners with an account at the issuer of stablecoins can convert at par on demand but with restrictions (approval) and after payment of a fee, whereas retail owners must convert on exchanges where de-pegging can and has occurred.” [20] (own emphasis)

The widespread adoption of dollar-backed stablecoins within Europe hence has the potential to increase the geopolitical risk as this ‘would expose European payments to US monetary policy’, a risk that is currently being contained in the EU by the following features:

“Europeans have broad access to euro-denominated payments and deposits,

inflation is relatively stable and low, and

MiCA allows the ECB to halt the issuance of USD-stablecoins if they become

systemically large.” [21]

Nonetheless,

Murau, S. (2017) ‘Shadow money and the public money supply: the impact of the 2007-2009 financial crisis on the monetary system’, in Review of International Political Economy, Vol. 24 (5), pp. 802-838.

Murau, S. (2017) ‘The Political Economy of Private Credit Money Accommodation: A Study of Bank Notes, Bank Deposits and Shadow Money’,

Wullweber, J. (2019) ‘Embedded Finance: The Shadow Banking System, Monetary Politics and Sovereign Power’

…

Digital Currency

Central Bank Digital Currency (CBDC)

Bindseil and Senner (2025a), “Revisiting national, economic, and monetary sovereignty”, [online] available at: <https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5486546> [Last accessed on 28th August 2025].

Bindseil and Senner (2025b), “Coordination, Contingency and Coercion: Monetary Sovereignty from Gold to the Dollar”, [online] available at: <https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5717544> [Last accessed on 28th August 2025].

Westermeier, C. & Hengsbach, D. (2025) ‘Geld als politische Technologie — Staat-Markt-Beziehungen im digitalen Euro’, in Huhnholz, S., Sahr, A. & Weiler, E. (Hrsg.) Politische Theorien öffentlicher Finanzen: Zur (De-)Politisierung von Geld, Eigentum und Steuern, Leviathan Sonderband 43, Baden-Baden: Nomos, pp. 257-283.

The outcome of this co-developing evolution is that the

“acceptability for some new privately-issued liabilities has been built upon a set of legal rules that nowadays most jurisdictions share. There is, therefore, no clear opposition between private and public money but rather different ways of mutual entanglement.” [x]

…dialectic of state and capital (Arrighi, 2010)

the one really essential characteristic of money is that the holder should be able to get rid of it without undue loss // money never finds an ultimate destination or resting-place (it circulates from person to person) - Young (1929/1924), p. 266

<https://podurama.com/episode/7233a6fa-1356-5ce3-9a5d-47a9f6986359>

Sources:

[1] Jazewitz, S. A. (2025) ‘Stablecoins Could Increase Treasury Demand, but Only by Reducing Demand for Other Assets’, in Federal Reserve Bank of Kansas City’s Economic Bulletin, [online] available at: <https://www.kansascityfed.org/research/economic-bulletin/stablecoins-could-increase-treasury-demand-but-only-by-reducing-demand-for-other-assets/> [Last accessed on 28th August 2025].

[2] Bundesbank (2017) ‘Die Rolle von Banken, Nichtbanken und Zentralbank im Geldschöpfungsprozess’, in Monatsbericht 69/4, pp. 15-36, [online] available at: <https://www.bundesbank.de/resource/blob/614448/c0acb63e33120467bbb3615c63dc7ea/mL/2017-04-%20%20%20geldschoepfungsprozess-data.pdf> [Last accessed 18th February 2023].

[3] Holmes, A. R. (1969) ‘Operational Constraints on the Stabilization of Money Supply Growth’, in Boston FED Controlling Monetary Aggregates, p. 73, [online] available at: <https://www.bostonfed.org/-/media/Documents/conference/1/conf1i.pdf> [Last accessed 2nd January 2025].

[4] Daniele M. (2025) ‘(A)STABLECOINS PART 1’, [online] available at: <https://www.linkedin.com/posts/daniele-m-4a2175221_unstablecoins-parte1-molti-pensano-che-activity-7393958225395486721-DMTn?utm_source=share&utm_medium=member_desktop&rcm=ACoAABroZAoBTLZgkbFWD4REGeRZ7l-APZhaFwI> [Last accessed on 12th November 2025].

[5] Ibid.

[6] EBA (2025) Crypto assets explained, [online] available at: <https://www.eba.europa.eu/sites/default/files/2025-10/0b10e48a-1a95-404c-b771-8bdb6503aac1/Updated%20Joint%20ESAs%20Factsheet%20on%20crypto-assets_EN.pdf> [Last accessed 27th November 2025].

[7] Binder, A. (2025) ‘Staatsfinanzen und Offshore Finanz’, in Huhnholz, S., Sahr, A. & Weiler, E. (Hrsg.) Politische Theorien öffentlicher Finanzen: Zur (De-)Politisierung von Geld, Eigentum und Steuern, Leviathan Sonderband 43, Baden-Baden: Nomos, p. 196.

[8] Ricks, M. (2016) The money problem: Rethinking financial regulation, Chicago, IL: University of Chicago Press, as cited in: Braun, B., Krampf, A. and Murau, S. (2021) ‘Financial globalization as positive integration: monetary technocrats and the Eurodollar market in the 1970s’, in Review of International Political Economy, Vol. 28 (4), p. 798.

[9] Binder, A. (2025) ‘Staatsfinanzen und Offshore Finanz’, in Huhnholz, S., Sahr, A. & Weiler, E. (Hrsg.) Politische Theorien öffentlicher Finanzen: Zur (De-)Politisierung von Geld, Eigentum und Steuern, Leviathan Sonderband 43, Baden-Baden: Nomos, pp. 196.

[10] Ibid., pp. 196f.

[11] Wullweber, J. (2024) Central Bank Capitalism, Stanford, CA: Stanford University Press, p. 51.

[12] Ricks, M. (2016) The money problem: Rethinking financial regulation, Chicago, IL: University of Chicago Press, p. 34.

[13] Ibid.

[14] Ibid.

[15] Ibid., p. 35 and corresponding footnote 12 explained on pp. 270f.

[16] Ibid., p. 36.

[17] Braun, B., Krampf, A. & Murau, S. (2021) ‘Financial globalization as positive integration: monetary technocrats and the Eurodollar market in the 1970s’, in Review of International Political Economy, Vol. 28 (4), pp. 798f.

[18] Barbat-Layani, M.-A. (2025) ‘EU watchdog must be given more power over fund managers, markets’, in Financial Times, December 1, [online] available at: <https://www.ft.com/content/c0e103c8-b4cd-4eba-8568-9f6662d9ddbd> [Last accessed 2nd December 2025].

[19] Singh, O. (2025) ‘Why USDC Can’t Be One Global Token Under Both MiCA and the US GENIUS Act’, [online] available at: <https://www.msn.com/en-us/money/markets/why-usdc-can-t-be-one-global-token-under-both-mica-and-the-us-genius-act/ar-AA1QSIL4> [Last accessed 2nd December 2025].

[20] Gabor, D. (2025) ‘Transatlantic Fault Lines: Risks and opportunities in the EU-US macro-financial relations’, in European Parliament Think Tank, p. 31, [online] available at: <https://www.europarl.europa.eu/thinktank/en/document/ECTI_STU(2025)764372> [Last accessed on 25th November 2025].

[21] Monnet, E. (2025) ‘Introductory statement by Éric Monnet to the public hearing held by the Committee on Economic and Monetary Affairs (ECON) on “Digital assets - challenges for the competitiveness and integrity of the EU’s financial system” on Wednesday, 3 December 2025, from 11:00 to 12:30.’, [online] available at: <https://www.europarl.europa.eu/cmsdata/300905/Eric%20Monnet.pdf> [Last accessed on 8th December 2025].

[x] Tropeano, D. (2025) ‘New Private Forms of Money and the State’, in International Journal of Political Economy, Vol. 54 (2), p. 231.

Arrighi, G. (2010) [1994] The Long Twentieth Century: Money, Power and the Origins of our Times, London: Verso.

[y] Young, A. (1929/1924) ‘The mystery of money: How modern methods of making payments economize the use of money. The role of checks and bank-notes’, in The Book of Popular Science, New York, NY: The Grolier Society, pp. 265-276.

Menand, L. & Younger, J. (2023) ‘Money and the Public Debt: Treasury Market Liquidity as a Legal Phenomenon’, in Columbia Business Law Review, Vol. 2023 (1), pp. 224-337.

Murau, S. (2017) ‘Shadow money and the public money supply: the impact of the 2007-2009 financial crisis on the monetary system’, in Review of International Political Economy, Vol. 24 (5), pp. 802-838.

Murau, S. (2017) ‘The Political Economy of Private Credit Money Accommodation: A Study of Bank Notes, Bank Deposits and Shadow Money’, Doctoral Thesis, London: University of London, [online] available at: <https://openaccess.city.ac.uk/id/eprint/19010/> [Last accessed on 28th August 2025].

Murau, S. & Pforr, T. (2020) ‘Private Debt as Shadow Money? Conceptual Criteria, Empirical Evaluation and Implications for Financial Stability’, [online] available at SSRN: <https://ssrn.com/abstract=4264552> [Last accessed on 28th August 2025].

Wullweber, J. (2019) ‘Embedded Finance: The Shadow Banking System, Monetary Politics and Sovereign Power’, [online] available at SSRN: <https://ssrn.com/abstract=3431909> [Last accessed on 28th August 2025].

Tropeano, D. (2020) ‘Does the BRRD affect the retail banking business model in the Euro area?’, in Economic Notes, [online] available at: <https://doi.org/10.1111/ecno.12162> [Last accessed on 28th August 2025].

Stellinga, B. et al. (2021) ‘The History of Money Creation’, in Money and Debt: The Public Role of Banks.

Braun, B., Krampf, A. & Murau, S. (2020) ‘Financial globalization as positive integration: monetary technocrats and the Eurodollar market in the 1970s’, in Review of International Political Economy, Vol. 28 (4), pp. 794-819.

Sahr, A. (2026) Fake Coins, Hamburg: Verlag des Hamburger Instituts für Sozialforschung.

___

Di Muzio, T. and Robbins, R. H. (2017) ‘Theory, History and Money, in An Anthropology of Money, New York, NY: Routledge.

Aglietta, M. (2018) [2016] Money: 5,000 Years of Debt and Power, London: Verso.

Stablecoins

“(A)STABLECOINS PART1

Many think that stablecoins increase the demand for Treasuries, thus supporting the market. Stablecoins issuers currently represent only a small part of the Treasury market. The entire US dollar stablecoin market is around $250 billion. However, not all assets are held in Treasuries. Stablecoins issuers currently hold about $125 billion in Treasuries (the US public debt is $38 trillion). Obviously, this figure could increase in the future. J.P. Morgan, for example, estimates that the stablecoin market could reach $500 billion by 2028.

That said, the important question is: do stablecoins really increase demand for Treasuries?

A Federal Reserve paper on stablecoins states: “Funds flowing into stablecoins have to flow out of another source ... This potential flow of funds from bank deposits into stablecoins could increase Treasury demand but also could reduce the supply of loans in the economy.”

This statement is completely wrong. Stablecoins are assumed to increase demand for Treasuries and decrease lending by banks. As far as loans are concerned, we are at the usual with the “loanable funds theory”. When will they stop teaching it? Banks do not lend deposits. Banks do not lend reserves. Banks create loans and deposits at the same time. The fact that a customer of the bank decides to buy stablecoins with his deposits does not diminish the bank’s chances of creating new loans at all. So buying stablecoins with deposits does not decrease lending by banks.

It was also claimed that stablecoins increase the demand for Treasuries. This is also false. When talking about these topics, it is necessary to use accounting passages to avoid saying rubbish. Let’s take an example.

A private investor (Goofy) buys $100 worth of stablecoins. The stablecoins issuer “collects” deposits and then buys Treasuries on the secondary market. However, this means that someone (Marta) is selling Treasuries and “cashing” deposits. At the aggregate level, nothing changes. The deposits have moved from one private (Pippo) to another (Marta). Treasuries moved from a private individual (Marta) to the stablecoins issuer. So buying stablecoins with deposits does not increase the demand for Treasuries. It is an asset swap.

Others argue that buying stablecoins can “drain” deposits from the banking system. In the example just presented this does not happen (asset swap). This can only happen in one case, which we will see in (UN)STABLECOINS PART2.”

Daniele M. (2025) ‘(A)STABLECOINS PART 1’, [online] available at: <https://www.linkedin.com/posts/daniele-m-4a2175221_unstablecoins-parte1-molti-pensano-che-activity-7393958225395486721-DMTn?utm_source=share&utm_medium=member_desktop&rcm=ACoAABroZAoBTLZgkbFWD4REGeRZ7l-APZhaFwI> [Last accessed on 12th November 2025].

Complementary addition to the sources for the charts on US dollar-denominated gross money-claim figures as provided by Morgan Ricks (2016, pp. 50f) - Appendix:

Sovereign Money-Claims:

- Currency in circulation. Source: Federal Reserve Economic Database, series MBCURRCIR.

- Federal Reserve balances. Source: Federal Reserve Economic Database, series BOGMBBM.

- Insured deposits. The series represents insured deposit obligations of all FDIC-insured institutions. The maturity breakdown is not available. The series may therefore include some certificates of deposits with maturities longer than one year, but it is unlikely that the amounts are large. Sources: FDIC Quarterly Banking Profile, 4Q’13 (for 2010– 13), 4Q’09 (for 2006– 9), 4Q’05 (for 1999–2005), and 4Q’01 (for 1995– 98).

- Treasury bills. Source: Economic Report of the President (2014), table B- 25.

Private Money-Claims:

- Repurchase agreements (“repo”). A repo transaction consists of the sale of a security coupled with an agreement to buy the security back at a slightly higher price. It is economically equivalent to a secured borrowing. The series represents repo obligations of the primary dealers. The maturity breakdown is not available. The series may therefore include some repo instruments with terms longer than one year, but it is unlikely that the amounts are significant. Sources: Financial Stability Oversight Council, 2014 Annual Report (for 2011– 13) and 2011 Annual Report (for 1995– 2010).

- Asset-backed commercial paper. Asset- backed commercial paper consists of short-term IOUs issued by special- purpose conduits, including structured investment vehicles, that invest in longer- term bonds (typically structured credit). Sources: Federal Reserve Economic Database, series ABCOMP (for 2001– 13); Federal Reserve Data Download Program (for 1995– 2000).

- Financial commercial paper. The series represents commercial paper issued by financial institutions. Sources: Federal Reserve Economic Database, series FINCP (for 2001– 13); Federal Reserve Data Download Program (for 1995–2000).

- Nonfinancial commercial paper. The series represents commercial paper issued by nonfinancial firms. Sources: Federal Reserve Economic Database, series COMPAPER (for 2001– 13); Federal Reserve Data Download Program (for 1995– 2000).

- Securities lending collateral IOUs. In a typical securities lending transaction, an asset manager lends a security to a third party, who then sells the security with the expectation of buying it back later at a lower price (shorting) and then returning it to the asset manager. Securities borrowers post cash collateral with securities lenders. Securities lenders usually reinvest the collateral rather than holding it on a custodial basis. They thereby incur what amounts to a demandable debt obligation. Sources: Financial Stability Oversight Council, 2014 Annual Report (for 2013) and 2013 Annual Report (for 1995– 2012).

- Eurodollars. Eurodollars are dollar- denominated short- term IOUs that are issued by financial institutions domiciled outside the United States. Reliable estimates of the size of the Eurodollar market are hard to come by. A recent study reports dollar deposits of banks outside the United States of $4.1 trillion as of year- end 2008.59 My Eurodollar estimate is $4.2 trillion at that date.

One textbook estimates a Eurodollar market size of “more than $5 trillion in the first decade of the 2000s.” My series peaked at $4.9 trillion in 2007. A 1998 study estimated $1.5 trillion in Eurodollars as of 1996, based on unspecified data from the International Securities Market Association. My estimate for 1996 is likewise $1.5 trillion. My data series is derived from global bank data compiled by the Bank for International Settlements (BIS). It consists of the product of (1) banks’ dollar- denominated cross- border liabilities that are designated as foreign currency liabilities and (2) the ratio of (A) banks’ consolidated outstanding international claims up to and including one year for all countries and (B) banks’ total consolidated outstanding international claims for all countries. Source: BIS Banking Statistics, tables 5A, 9A(A), and 9A(B).

- Uninsured deposits. The series represents the difference between (1) the sum of total checkable deposits (series TCDNS), small time deposits (series STDNS), savings deposits (series SAVINGNS), and large time deposits (series LTDACBM027NBOG), all from Federal Reserve Economic Database, and (2) insured deposits (see above). The maturity breakdown is not available. The series may therefore include some time deposits with maturities longer than

one year, but it is unlikely that the amounts are large.

- Money market fund shares— retail. Source: Federal Reserve Economic Database, series RMFNS.

- Money market fund shares— institutional. Source: Federal Reserve Economic Database, series IMFNS.