Critical Appraisal of the Theories of Banking

The theories of banking revisited: "payment" vs. "funding"

The theories of banking introduced so far follow a typology proposed by Richard A. Werner: [1]

The Credit Creation Theory of Banking = FMC (III).

Werner rejects the “intermediation of loanable funds” (ILF) theory (I) and the “fractional reserve circulation” (FRC) model (II) while promoting the “financing through money creation” (FMC) model (III) as the only correct one. The importance of their empirical validity should not be underrated. As Werner highlights the fact that the ILF model (I) serves as the current foundation for capital adequacy-based bank regulation, this has real-world repercussions on the effectiveness of economic modelling and financial policy-making. [2]

For context:

The FMC model of banking (III) can be viewed as a conceptualisation of the liquidity-oriented strain of monetary theory whereas the ILF model of banking (I) is most likely to be categorised under the money-supply related strain. [3]

This debate goes as far back as the mid-1800s when the British Currency School represented the latter and the British Banking School the former view. [4]

Further criticisms:

It is misleading that banks hold the position of (pure) financial intermediaries (I), when it is believed that they are merely able to award loans if they issued savings deposits to other customers beforehand. [5]

In reality, it is the case that banks’ key function is the provision of financing (III) ‘or the creation of new monetary purchasing power through loans, for a single agent that is both borrower and depositor. Banks therefore create their own funding deposits, in the act of lending, in a transaction that involves no intermediation whatsoever’. [6]

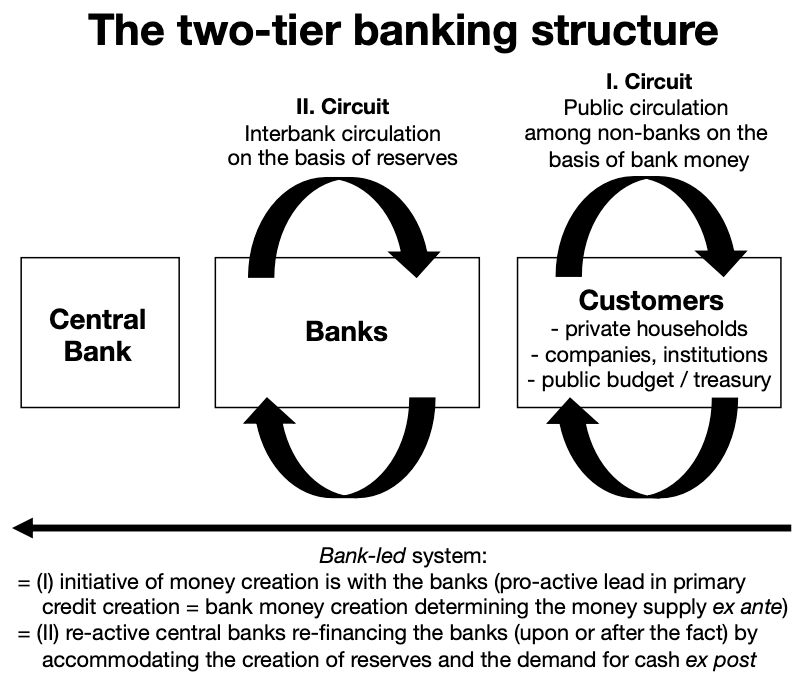

However, Joseph Huber would contend that under the present system banks are involved with managing two monetary circuits that circulate separately but nonetheless do interdependent on each other. [7]

“Money is unique in that it is created in the act of financing by a bank and is destroyed as the commitments on debt instruments owned by banks are fulfilled. Because money is created and destroyed in the normal course of business, the amount outstanding is responsive to the demand for financing. Banks are important exactly because they do not operate under the constraint of a money lender - banks do not need to have money on hand in order to lend money. This flexibility of banks means that projects in need of funds over an extended period of time can arrange for such funds to be available as needed. A line of credit and a commitment by a bank are as good as the possession of funds.” [8] (own emphasis)

This quote from Hyman P. Minsky highlights a monetary system’s need for elasticity in order for it to be responsive enough to the demand for financing. The ILF (I) and the FRC (II) models do not incorporate this since they presume initial saving activity on the one hand (I) or theorise central banks to regulate the (base) money supply via the initial extension of reserves to banks on the other hand (II), both limiting the scope of elasticity (and velocity) in the system.

According to the above figure (based on Huber), banks do create deposits in the act of lending (III) — but are dependent on central banks accommodating their need to re-finance by providing them with a market for central bank reserves, i.e. reversing FRC (II).

When the ‘money multiplier’ theory asserts that ‘banks are lending out existing deposits and that the banking system creates new money as money passes from bank to bank in the form of deposits and loans’, the FRC model (II) does not completely explain:

the creation of money needed for the initial deposit;

the accounting procedure if banks lend a portion of their deposits that they are not required to keep in reserve, as money cannot be in two places at once, i.e. it merely describes the redistribution of existing money; and

hence the expansion of the money supply. [9]

It is an attempt to explain the dimunition of money and its eventual disappearance from the economy as it is held by banks as reserves, but if money was created by loaning out a percentage of deposits while not subtracting the amount from the bank’s liabilities, the banking system would have no justifiable credibility. [10]

The Great Recession has shown, however, that the monetary base has increased in many countries enormously without the effect of an expansion of the money supply, i.e. the amount of loans.

The ‘money multiplier’ approach further implies a causality that a higher monetary base leads to a higher money supply in that central banking is thought to be able to expand the amount of loans and therefore the amount of money in the economy by simply raising the monetary base, i.e. cash and reserves held by commercial banks at central banks. [11]

Limitations on the money supply and/or credit expansion:

Economists at the Bank of England contend that the FRC model (II) is also not accurate since in reality central banks today implement monetary policy by determining the price of reserves — that is, through adjusting interest rates:

“In reality, neither are reserves a binding constraint on lending, nor does the central bank fix the amount of reserves that are available. As with the relationship between deposits and loans, the relationship between reserves and loans typically operates in the reverse way to that described in some economics textbooks. Banks first decide how much to lend depending on the profitable lending opportunities available to them — which will, crucially, depend on the interest rate set by the Bank of England. It is these lending decisions that determine how many bank deposits are created by the banking system. The amount of bank deposits in turn influences how much central bank money banks want to hold in reserve (to meet withdrawals by the public, make payments to other banks, or meet regulatory liquidity requirements), which is then, in normal times, supplied on demand by the Bank of England.” [12] (own emphasis)

Lending is not only being restricted by reserve holdings of commercial banks at the central bank’s account. Key factors are loan demand in a highly competitive branch of the economy as much as expenditure and earnings calculus and micro-/macro-prudential regulations such as regulatory capital limits, for instance, set by financial authorities and international accounting standards. [13]

Furthermore can be noted that central banks understand themselves as steering the process of credit money origination through their main interest rates and thus indirectly via interest rates on the money market. As lending by banks functions primarily with the aim of profit maximisation with the difference between the interest rate for bank loans and the central bank’s interest rate (corresponding broadly with the money market interest rate) taking up a central role.

More limitations are the availability of willing borrowers that are likely to repay the principal including the added interest; decisions by banks to stop lending in uncertain economic conditions where the risk of default looks high; that borrowers may use new funds to pay off old debts, effectively removing new money from circulation and lastly, for adjusting the money supply in equilibrium it is the central bank that makes the necessary monetary base passively available: causality is from (credit) money supply to monetary base (reserves) and not vice versa. [14]

As such, (minimum) reserve requirements have little to no effect on lending as there is no reserve constraint on lending and banks never make loans to customers depending on their reserves (many countries like Australia, New Zealand, the UK, Sweden and Canada do not have a reserve requirement at all, for instance). The only link between bank lending and reserves is that ‘reserves go down when banknotes increase’. [15]

Also problematic is the fact that banks do not create the issued interest when granting loans to supposedly credit-worthy counter-parties — meaning that this explains the crisis-prone symptom of there being always more debt in the system than there is the ability to repay: [16]

“If we take a cross-section of the flow of purchasing power delivered to the buying public in the form of wages, salaries, and dividends, and at the same moment take a cross-section of the flow of prices, we shall find that the latter cross-section is always greater than the former.” [17]

Final appraisal:

Huber criticises Werner’s reading of the FRC model (II) as it represents ‘an incomplete and partially inadequate understanding of reserve circulation’. [18] It combines reserve banking (II) with the loanable funds model (I) and equates that combination with the multiplier model and the reserve position doctrine. [19]

The FMC model (III) on bank money creation (out of nothing) ‘is all too unspecific and overstated, blinding out the connection of bank money with reserve circulation’:

“this does not justify reducing fractional reserve circulation to that mishmash and then presenting fractional reserve banking and bank credit creation as 'mutually exclusive views', while in actual fact both elements – bank credit creation, and fractional reserve circulation – go hand in hand.” [20]

Perry Mehrling also is wary of seeing the three theories of banking as ‘quite as mutually exclusive’, since it is the ‘distinction between “payment” and “funding”’ that is the central analytical puzzle to be concerned with. [21] (own emphasis)

He argues that the ILF model (I) can be in some instances ‘perfectly consistent’ with the FMC model (III) in that (I) focuses on the ultimate funding whereas (III) focuses on the initial payment. [22]

Last but not least, the avid reader, by following the trail of the sources extensively made reference to, may have recognised that a good number of central banks have published papers to shed more light on the issue of money creation. The Reserve Bank of New Zealand recently joined in and summarised the present monetary system as follows:

“The vast majority of money in circulation is created by commercial banks, through the process of bank lending. The Reserve Bank has direct control over the settlement cash level, but this only has an indirect influence on the quantity of broad money in the economy, and is not particularly relevant for the transmission of monetary policy under the current framework.” [23]

To close this discussion, it may be worth to conceive of the epistemological merit of engaging with each theory critically and still allow for acknowledgement of their overall contribution to economic thought.

Primary knowledge interest:

(I) intermediation: most efficient allocation of resources

(II) fractional reserve: monetary policy transmission

(III) credit creation: connection (but no congruence) between money and debt

Sources:

[1] Werner, R. A. (2016) ‘A lost century in economics: Three theories of banking and the conclusive evidence’, in International Review of Financial Analysis, Vol. 46, pp. 361-379.

[2] Ibid., p. 361.

[3] Claassen, E.-M. (1980) Grundlagen der Geldtheorie, 2nd ed., Berlin: Springer, Chapter 1.

[4] Cramp, A. B. (1962) ‘Two Views on Money’, in Lloyds Bank Review, No. 65, pp. 1-15.

[5] Bundesbank (2017) ‘Die Rolle von Banken, Nichtbanken und Zentralbank im Geldschöpfungsprozess’, in Monatsbericht 69/4, pp. 15-36, [online] available at: <https://www.bundesbank.de/resource/blob/614448/c0acb63e33120467bbb3615c63dc7ea/mL/2017-04-%20%20%20geldschoepfungsprozess-data.pdf> [Last accessed 18th February 2023].

[6] Kumhof, M. and Zoltán, J. (2015) ‘Banks are not intermediaries of loanable funds — and why this matters’, in Working Paper No. 529, London: Bank of England, p. ii, [online] available at: <https://www.bankofengland.co.uk/-/media/boe/files/working-paper/2015/banks-are-not-intermediaries-of-loanable-funds-and-why-this-matters.pdf> [Last accessed 18th February 2023].

[7] Huber, J. (2017) Sovereign Money: Beyond Reserve Banking, Cham, CH: Palgrave Macmillan, pp. 57f.

[8] Minsky, H. P. (2008/1986) Stabilizing an Unstable Economy, New York, NY: McGraw-Hill, p. 278.

[9] Di Muzio, T. and Noble, L. (2017) ‘The Coming Revolution in Political Economy: Money, Mankiw and Misguided Macroeconomics’, in Real-World Economics Review, Vol. 80, pp. 85-108.

[10] Ibid.

[11] Bofinger, P. (2017) ‘Realwirtschaftliche Modelle sind überholt’, in FAZIT – das Wirtschaftsblog, [online] available at:<https://blogs.faz.net/fazit/2017/07/19/realwirtschaftliche-modelle-sind-ueberholt-8932/> [Last accessed 18th February 2023].

[12] McLeay, M., Radia, A. and Thomas, R. (2014) ‘Money creation in the modern economy’, in Quarterly Bulletin 2014 Q1, pp. 14-27 (p. 15), [online] available at: <https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/2014/money-

creation-in-the-modern-economy> [Last accessed 18th February 2023].

[13] Bundesbank (2017) ‘Die Rolle von Banken, Nichtbanken und Zentralbank im Geldschöpfungsprozess’, in Monatsbericht 69/4, pp. 15-36, [online] available at: <https://www.bundesbank.de/resource/blob/614448/c0acb63e33120467bbb3615c63dc7ea/mL/2017-04-%20%20%20geldschoepfungsprozess-data.pdf> [Last accessed 18th February 2023].

[14] Di Muzio, T. and Noble, L. (2017) ‘The Coming Revolution in Political Economy: Money, Mankiw and Misguided Macroeconomics’, in Real-World Economics Review, Vol. 80, pp. 85-108.

[15] Ibid.

[16] Ibid.

[17] Douglas, C. H. (1931) The Monopoly of Credit, London: Chapman and Hall, pp. 160f.

[18] Huber, J. (2016) ‘Critical remarks on R. Werner's typology of banking models’, [online] available at: <https://sovereignmoney.site/werner-typology-of-banking-theories> [Last accessed 10th February 2023].

[19] Ibid.

[20] Ibid.

[21] Mehrling, P. (2016) ‘“Great and mighty things which thou knowest not” [?]’, [online] available at: <https://sites.bu.edu/perry/2016/01/27/great-and-mighty-things-which-thou-knowest-not/> [Last accessed 10th February 2023].

[22] Ibid.

[23] Knowles, J., Austin, L. and Kerr, L. (2023) ‘Money Creation in New Zealand’, in Bulletin, Vol. 86 No. 1, pp. 1-16, [online] available at: <https://www.rbnz.govt.nz/hub/-/media/project/sites/rbnz/files/publications/bulletins/2023/money-creation-in-new-zealand.pdf> [Last accessed 18th February 2023].

AI is quite chartalist in its take to explain the process of money creation: https://mastodon.social/@alexio/110114412357120561