The Fractional Reserve Theory of Banking

A brief introduction to a widely referred theory of banking

Image created with Copilot (2025).

The fractional reserve theory of banking promotes the view that the banking sector as a whole is able to create deposits on the basis of being granted access to new reserves at the central bank. The reserves provide liquidity (checkbook deposits) for cash withdrawals (currency in circulation) provided that the banking system is not under stress during times of crisis (as is the case for bank runs) — hence the term fractional reserve banking. This theory is closely entangled with the money multiplier approach.

Main assumptions:

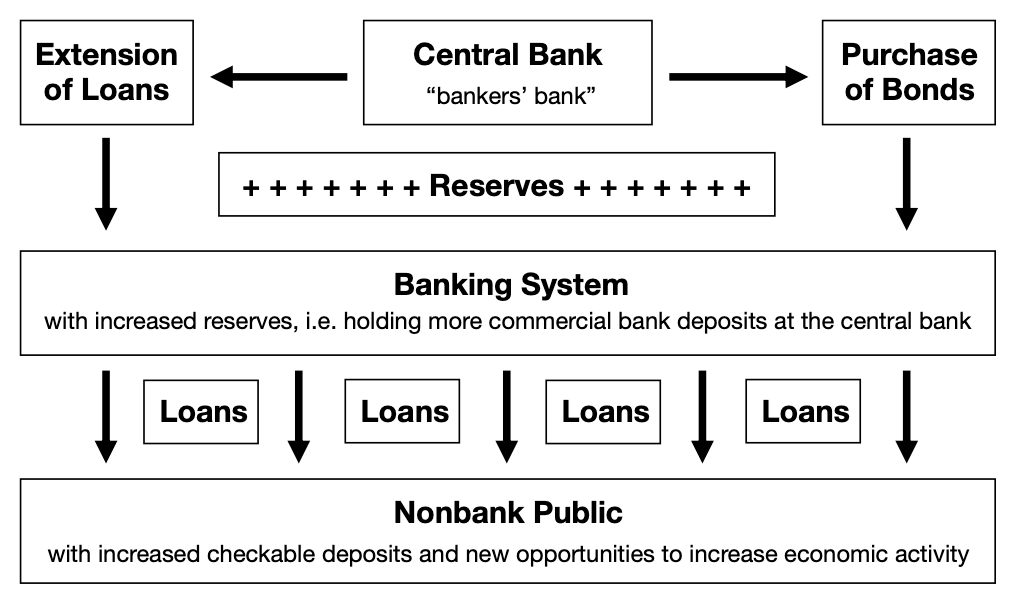

central banks (first) create reserves through:

open market purchases of government bonds

their extension of discount loans to banks

private commercial banks (then) utilise additional supply of reserves to transform them into more money by lending on a share of collected deposits (minus reserve requirement)

deposit expansion rests thus on the need for their full and prompt utilisation

Historical formation & development:

As the here presented theory of money creation is the result of a long evolutionary process, the standard explanation for the development of fractional reserve banking commonly traces back to the myth of the goldsmith bankers during the 17th century and before [1]:

“It became customary for people who had gold to deposit it with the goldsmiths for safekeeping. The goldsmith then gave the depositor a "claim check," or a receipt, for his gold. In time these receipts became transferable. Anyone having possession of a receipt was supposed to be able to go to the goldsmith and claim the gold. What actually happened was that these receipts for gold began circulating as money. People learned that they could carry on trade and commerce by passing goldsmith's receipts from hand to hand without ever drawing out the gold. This led the goldsmith to a discovery which has been the principle of banking ever since "fractional reserves." […] In other words, the goldsmith wrote receipts for people who were not depositing gold. These receipts too circulated as money. So receipts for more gold than the goldsmith actually had in his vaults were circulating. The goldsmith had only a fraction of the amount of gold needed to meet the claims against him. This is the fractional reserve system.” [2] (original emphasis)

Textbooks further like to present central banks as having the capacity to determine the quantity of loans and deposits in the economy by controlling the quantity of central bank money — the so-called ‘money multiplier’ approach.

Mishkin, Matthews & Giuliodori, 2013, p. 307:

“When the central bank supplies the banking system with a certain amount of additional reserves, deposits increase by a multiple of this amount – a process called multiple deposit creation.” [3]

Mankiw, 2016, pp. 94-101:

“Each dollar of the monetary base produces m dollars of money. Because the monetary base has a multiplied effect on the money supply, the monetary base is sometimes called high-powered money. […] Although it is often convenient to make the simplifying assumption that the Federal Reserve controls the money supply directly, in fact the Fed controls the money supply indirectly using a variety of instruments. These instruments can be classified into two broad groups: those that influence the monetary base and those that influence the reserve-deposit ratio and thereby the money multiplier. […] The money multiplier depends on the reserve-deposit ratio, which in turn is influenced by various Fed policy instruments. […] The system of fractional-reserve banking creates money because each dollar of reserves generates many dollars of demand deposits. […] The supply of money depends on the monetary base, the reserve-deposit ratio, and the currency-deposit ratio. An increase in the monetary base leads to a proportionate increase in the money supply. A decrease in the reserve-deposit ratio or in the currency-deposit ratio increases the money multiplier and thus the money supply. The Federal Reserve influences the money supply either by changing the monetary base or by changing the reserve ratio and thereby the money multiplier. It can change the monetary base through open-market operations or by making loans to banks. It can influence the reserve ratio by altering reserve requirements or by changing the interest rate it pays banks for reserves they hold.” [4]

Burda & Wyplosz, 2013, p. 211f:

“[C]ommercial banks set aside 10% of any money deposited on their customers’ accounts. Presumably, they kept it in the form of cash—which often requires an expensive and secure (robber-proof) vault. The more convenient alternative to this is to deposit these amounts with the central bank. […] [B]y choosing the volume of reserves, the central bank can control total bank deposits. Since M=currency in circulation+bank deposits and the central bank precisely sets currency in circulation, central banks can control the money supply.” [5]

Purpose & ramifications:

legitimising banking as a maturity transforming, profitable business

theory contrasts with the idea of full-reserve banking (i.e. liabilities/loans being fully covered by a bank’s assets/deposits)

implicating a causality of an expansion of high-powered money leading automatically to increased lending activity by banks

Sources:

[1] Kindleberger, C. P. (1984) A Financial History of Western Europe, London: George Allen & Unwin, p. 51 citing Tawney, R. H. (1925, p. 102) and de Roover, R. (1949, p. 102).

[2] U.S. Committee on Banking and Currency (1964) A Primer on Money, Washington, D.C.: U.S. Government Printing Office, p. 28f.

[3] Mishkin, F. S., Matthews, K. and Giuliodori, M. (2013) The Economics of Money, Banking & Financial Markets: European Edition, Essex, UK: Pearson.

[4] Mankiw, N. G. (2016) Macroeconomics, 9th ed., New York, NY: Worth Publishers.

[5] Burda, M. and Wyplosz, C. (2013) Macroeconomics: A European Text, 6th ed., Oxford: Oxford University Press.