The Financial Intermediation Theory of Banking

The Financial Intermediation Theory of Banking

A sketchy introduction of the currently prevalent theory of banking

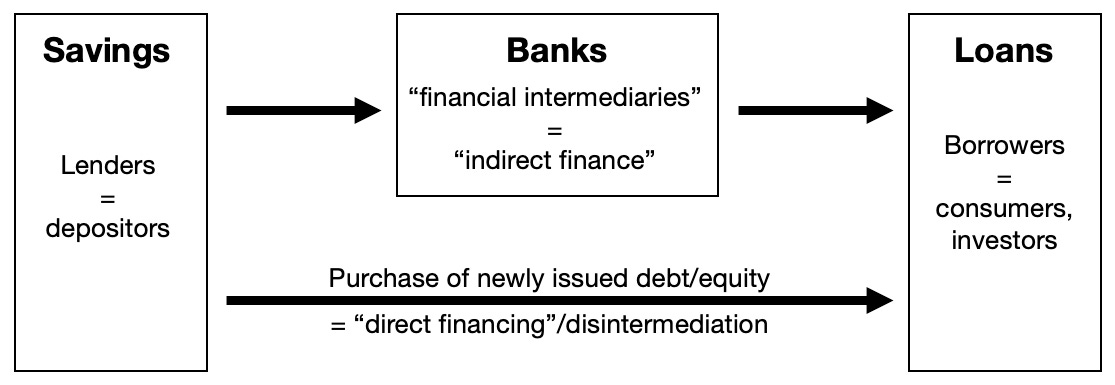

The financial intermediation theory of banking presents banks as financial intermediaries borrowing money from savers in order to lend demanded funds to loanees (who then either consume goods and services or invest in machinery, technology, in the advancement of enterprise). According to this theory banks provide “indirect finance” to its customers and clients contrary to the “direct financing” occurring on capital markets where those demanding funds collect them directly from investors (as money suppliers) thereby superseding banks — a process known under the term “disintermediation”. The model shown above contrasts the two possibilities of “external finance” (as opposed to “self-finance”) by showing the “indirect” financial intermediation of loanable funds through banks with the possibility of “direct financing” by the purchase of newly issued debt or equity.

Main assumptions:

banks only lend if they have gathered enough savings deposits beforehand, i.e. assuming a direct relationship between savings and loans (no new loans without prior savings)

banks are merely financial intermediaries, not different from other non-bank financial institutions

Historical formation & development:

The intermediation model was developed in the mid-1950s by John G. Gurley & E. S. Shaw:

“The role of the banks has been, first, to borrow loanable funds from spending units with surpluses, issuing indirect securities in exchange. […] The role of the banks has been, second, to transmit the borrowed funds to spending units with deficits, receiving in exchange direct securities for their own portfolios.” [1]

A good number of economics textbooks propagate further the view that banks are intermediaries in the sense that they appear to facilitate the movement of funds from non-bank creditors/savers to non-bank debtors/borrowers.

Mishkin, 2013, p. 78f:

“For example, a bank might acquire funds by issuing a liability to the public (an asset for the public) in the form of savings deposits. It might then use the funds to acquire an asset by making a loan to General Motors or by buying a U.S. Treasury bond in the financial market. The ultimate result is that funds have been transferred from the public (the lender-savers) to General Motors or the U.S. Treasury (the borrower-spender) with the help of the financial intermediary (the bank). The process of indirect finance using financial intermediaries, called financial intermediation, is the primary route for moving funds from lenders to borrowers.” [2]

Mishkin, Matthews & Giuliodori, 2013, p. 210f:

“In general terms, banks make profits by selling liabilities with one set of characteristics (a particular combination of liquidity, risk, size and return) and using the proceeds to buy assets with a different set of characteristics. This process is often referred to as asset transformation. For example, a savings deposit held by one person can provide the funds that enable the bank to make a mortgage loan to another person. The bank has, in effect, transformed the savings deposit (an asset held by the depositor) into a mortgage loan (an asset held by the bank). Another way this process of asset transformation is described is to say that the bank ‘borrows short and lends long’ because it makes long-term loans and funds them by issuing short-dated deposits. […] It does this by applying the ‘law of large numbers’ to liability management. Normally, depositors do not withdraw their deposits at the same time as other customers. Recognizing that depositors withdraw their funds at different times means that banks only need to hold a certain amount as reserves to meet day-to-day withdrawals and lend the rest in long-term loans. This process is known as maturity transformation.” [3]

Blanchard, 2017, p. 137:

“[M]uch of the borrowing and lending takes place through financial intermediaries, which are financial institutions that receive funds from some investors and then lend these funds to others. Among these institutions are banks, but also, and increasingly so, “non-banks,” for example mortgage companies, money market funds, hedge funds, and such.” [4]

Cecchetti & Schoenholtz, 2017, p. 270:

“[F]inancial institutions intermediate between savers and borrowers, and so their assets and liabilities are primarily financial instruments. Various sorts of banks, brokerage firms, investment companies, insurance companies, and pension funds all fall into this category. These are the institutions that pool funds from people and firms who save and lend them to people and firms who need to borrow, transforming assets and providing access to financial markets. They funnel savers’ surplus resources into home mortgages, business loans, and investments.” [5]

Purpose & ramifications:

development of macroeconomic models without a perceived need to account for the institutions and economic activities related to banking (“money as veil”)

establishment of a narrative of the benefits of frugality in economic conduct

bias towards balanced budgeting: facilitating the equation of private budgeting with public budgeting

Sources:

[1] Gurley, J. G. and Shaw, E. S. (1955) ‘Financial Aspects of Economic Development’, in The American Economic Review, Vol. 45, No. 4, pp. 515-538 (pp. 519f.).

[2] Mishkin, F. S. (2013) The Economics of Money, Banking, and Financial Markets, 10th ed., Essex, UK: Pearson.

[3] Mishkin, F. S., Matthews, K. and Giuliodori, M. (2013) The Economics of Money, Banking & Financial Markets: European Edition, Essex, UK: Pearson.

[4] Blanchard, O. (2017) Macroeconomics, 7th ed., London: Pearson.

[5] Cecchetti, S. G. and Schoenholtz, K. L. (2017) Money, Banking and Financial Markets, New York, NY: McGraw-Hill.